Are you making the most of your pension options? 5 common mistakes and how to avoid them

Dreaming of a comfortable retirement? It’s a goal shared by many, but navigating the complexities of pension planning can feel overwhelming.

Unfortunately, many people make easily avoidable mistakes that can significantly affect their retirement income.

These mistakes usually come from a lack of understanding or proactive planning and could jeopardise your financial security during what should be a time of relaxation and enjoyment.

I wanted to share with you some of the most common mistakes I see when it comes to pensions. More importantly, I’m going to provide several practical solutions to help you avoid them, aiming for a more secure and fulfilling retirement.

Here are my five top tips for avoiding mistakes and making the most of your pension options.

1. Not contributing enough to your pension could result in a shortfall

One of the most significant mistakes you could make pre-retirement is to not contribute enough to your pension.

The Institute for Fiscal Studies (IFS) reports that less than half of private sector employees who save into a workplace pension contribute more than 8%, which is the minimum requirement for most earners, with your employer being required to pay at least 3% of that.

Only making minimum contributions could make it more challenging to achieve a good standard of living in retirement.

In fact, the IFS goes on to state that around 30% – 40% of private sector employees saving into defined contribution (DC) pension schemes are on course to have individual incomes that fall short of standard retirement benchmarks.

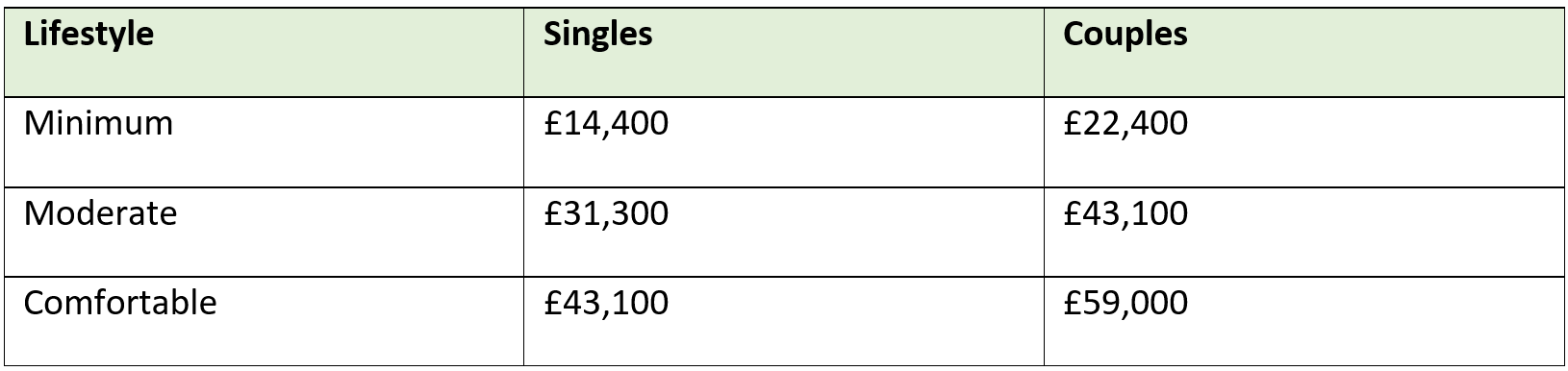

As it stands, the basic lifestyle requirements for retirement are as follows:

Source: Retirement Living Standards

Keep in mind that these figures can provide a helpful benchmark, but they are only estimates and individual needs and circumstances will vary. More than that, as prices increase with inflation, so too will the cost of living, meaning the same amount of money today won’t stretch as far in 10 years.

The Living Wage Foundation highlights this by stating that in 2023/2024, the average pension pot needed to meet basic needs had increased by 60% since 2020/2021.

Increasing your or your employer’s contributions, even by a small amount, can make a significant difference over time. Standard Life illustrates this by noting how even a 2% increase in employer contributions could boost your retirement savings by £115,000.

So, it’s important to assess your current contributions and determine if you’re on track to reach your preferred retirement lifestyle goals.

2. Misunderstanding tax on pension withdrawals can bring an unwelcome surprise

Another common mistake lies in misunderstanding the tax implications of your DC pension withdrawals. This includes most workplace pensions and self-invested personal pensions (SIPPs), but not defined benefit (DB) schemes, which come under different rules.

The first 25% you draw from a DC pension is usually tax-free, and you will normally pay Income Tax on the remaining 75%. By not taking this into account, you could face an unexpected tax burden when you begin drawing down your pension.

You will have two options when it comes to your 25% tax-free sum. You can either take it out as a lump sum when you retire, otherwise known as your “pension commencement lump sum” (PCLS), or spread it out over multiple withdrawals.

Keep in mind that your tax-free lump sum is capped by the Lump Sum Allowance (LSA). As of the 2024/2025 tax year, the LSA is £268,275. The LSA applies across all your pensions – you can take up to 25% of each pot tax-free, with the LSA limiting the total amount you can draw before facing a tax charge.

The amount you withdraw after your 25% tax-free amount will usually be combined with other sources of income you’re taking simultaneously, such as the State Pension, and taxed at your marginal rate.

For this reason, it’s important to factor in tax when you’re calculating your projected retirement income, whether you’re taking your full PCLS or withdrawing your money in parts. This is something I can help you with, and together we can work out a tax-efficient strategy for your retirement income.

3. Failing to regularly review your pension plan could affect your long-term outcomes

Life circumstances can change, and your retirement strategy should adapt accordingly. Changes in income, health, or even your retirement goals can require adjustments to your contributions, investment strategy, and withdrawal plans.

Put simply, a pension plan isn’t a “set it and forget it” exercise. It requires ongoing monitoring and adjustments to ensure it remains aligned with your evolving needs.

For example, if your income increases in the run-up to retirement, you might want to consider increasing your pension contributions. This could allow you to maintain your current standard of living in retirement or even retire earlier than you had initially planned. By contributing more when you can afford it and as your circumstances change, you could benefit more from the power of compound returns within your pension and build a larger retirement nest egg.

Conversely, if you experience a health issue or another setback such as divorce, you may need to adjust your retirement timeline or revisit your current withdrawal strategy.

Regular reviews allow you to make any necessary changes.

4. Not considering a pension consolidation plan could lead to lost gains

Though not necessarily the right move for everyone, it’s important to at least explore the idea of consolidating your pension pots.

If you’ve changed jobs multiple times, you likely have a few different pension pots. Managing these could involve extra admin and fees, but there may be benefits to keeping them, even if they’re small.

It’s important to avoid assuming that consolidation is always the most suitable option for you. If those smaller pensions are still performing well, or offer valuable benefits, then it may be worth leaving them as is. However, many find that consolidation offers a strong opportunity for compound returns.

This is a decision I can support you with, as I can help you compare fees and benefits, and offer guidance on which pots to keep, and what to consolidate.

5. Don’t underestimate the value of seeking professional advice

Many people underestimate the value of professional financial planning, but a qualified financial adviser can provide personalised guidance tailor-made for you. This could include everything from choosing the most suitable pension plan for you to optimising your withdrawal strategy.

In fact, Unbiased reports that those who receive professional financial advice have close to £48,000 more in pensions and other assets. More than that, those who had taken the advice of an expert were 61% better off overall.

Get in touch

By working together, we can get a full scope of your unique financial situation, risk tolerance, and retirement goals. From there, I can create a comprehensive plan that could maximise your chances of achieving a comfortable retirement.

Email Marnel.Stafford@fosterdenovo.com or call 07305 970959 or 0207 469 2800 to find out more about how I can help you.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance. Pension savings are at risk of being eroded by inflation.

Workplace pensions are regulated by The Pension Regulator.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation, and regulation, which are subject to change in the future.